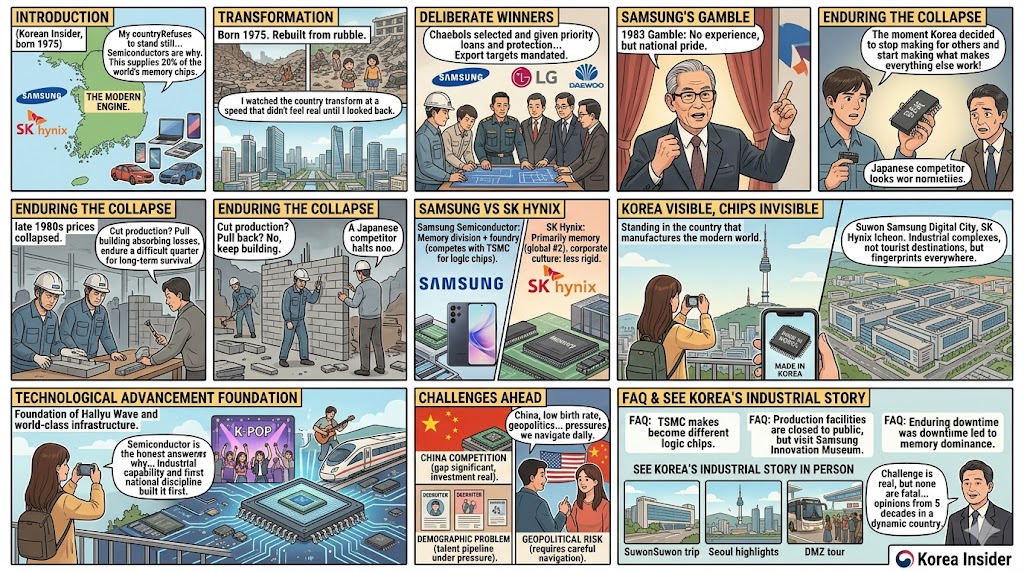

The Korean semiconductor industry supplies roughly 20% of the world’s memory chips. The DRAM in your laptop, the NAND flash in your phone, the memory module in your car’s navigation system — there’s a better-than-even chance it was made here, in South Korea, by either Samsung or SK Hynix.

I was born in Korea in 1975. My parents’ generation lived through the Korean War and rebuilt everything from rubble. My generation grew up watching the country transform at a speed that didn’t feel real until you looked back at it. And the semiconductor industry sits at the center of that transformation — not as a symbol, but as the actual engine. When people ask me what explains modern Korea, I usually start here, because almost everything else follows from it.

I’ve spent over 23 years working inside multinational corporations in Korea. I’ve sat in meetings with Samsung suppliers, worked alongside engineers from SK Hynix’s international divisions, and watched Korean chip production shape business decisions in boardrooms that had nothing to do with Korea. Here’s what I think the outside world consistently misses about how this actually happened.

The Numbers, Because They’re Genuinely Staggering

Korea controls approximately 70% of the global DRAM market and around 50% of NAND flash memory production. Samsung Semiconductor alone generates more annual revenue than the entire GDP of New Zealand. The semiconductor sector accounts for roughly 20% of Korea’s total exports — one in every five dollars Korea earns internationally comes from chips.

When the global chip shortage hit in 2021 and automakers started shutting down production lines, the world got a fast and uncomfortable education in just how much leverage Korea holds. That shortage wasn’t Korea’s fault — but Korea was where every phone call went looking for answers. That tells you everything about where the real power sits in the global supply chain.

How This Actually Happened

The version of this story that gets told in international business schools tends to make it sound inevitable. It wasn’t. It was a sequence of enormous bets that could have failed at multiple points, and understanding the real story matters — both for understanding Korea as a country and for understanding why the industry looks the way it does today.

The government chose its winners deliberately

My parents lived through the Park Chung-hee era. Whatever you think of the politics — and Koreans have complicated feelings about that period, myself included — the economic strategy was brutally focused. The government selected a small number of family-controlled conglomerates, the chaebols, and channelled preferential loans, contracts, and protection from foreign competition through them in exchange for meeting export targets.

Samsung, Hyundai, LG, Daewoo. These names didn’t become powerful by accident. They were, in a very deliberate sense, chosen. Growing up in Korea in the 1980s, the chaebols were simply the texture of the economy — they built the apartment blocks, made the appliances, ran the department stores. I didn’t fully understand until I started working in international business just how unusual this level of government-directed industrial concentration actually was by global standards. And just how much it compressed what might have taken other countries decades into a single generation.

Samsung’s 1983 gamble

In 1983, Samsung’s founder Lee Byung-chul announced the company would enter the semiconductor business. I was eight years old. I obviously don’t remember the announcement itself, but I grew up hearing the story told as a kind of national parable — the moment Korea decided it was going to stop making things for other people’s designs and start making the things that make everything else work.

At the time it was genuinely controversial. Samsung had no experience in semiconductors. The Japanese — Toshiba, NEC, Hitachi — were years ahead and operating at a different technical level entirely. My wife is Japanese, and she grew up with a completely different version of this story: the one where Korean engineers showed up in Tokyo to learn the industry and weren’t always welcome. The rivalry between Korean and Japanese semiconductor firms in the 1980s was real, sharp, and industrial — driven by national pride on both sides in ways that are impossible to fully separate from the history between the two countries.

Samsung produced its first 64K DRAM chip in 1983. Within a decade, it was the largest DRAM producer in the world.

The downturn that didn’t break them

Here’s the part of the story that usually gets glossed over. In the late 1980s, DRAM prices collapsed. Samsung was losing money on every chip it manufactured. The rational short-term decision was to cut production, pull back investment, wait for the market to recover.

Samsung kept building.

The company continued investing in capacity through the downturn, absorbing losses, betting that whoever came out the other side with the most production capacity would dominate the next cycle. The Japanese competitors who pulled back during that period never fully recovered their position. It is the same strategy Korea has run through every subsequent downturn — and it is why the industry looks the way it does today. When I see Korean companies absorbing short-term pain to capture long-term position, I recognize it as a pattern that runs much deeper than any individual business decision. It reflects something about how this country thinks about survival. My parents’ generation rebuilt a country from nothing. Enduring a difficult quarter feels different when that’s the frame of reference.

Samsung vs SK Hynix: The Actual Difference

Most people outside Korea treat these two names as interchangeable. They’re not.

Samsung Semiconductor is the memory division of Samsung Electronics — the same company behind your Galaxy phone and QLED television. It is the world’s largest producer of both DRAM and NAND flash, and it also operates a foundry business, manufacturing chips based on other companies’ designs. This is the division that competes directly with TSMC (Taiwan) for advanced logic chip production — a newer and strategically critical part of Samsung’s business.

SK Hynix focuses primarily on DRAM and NAND. Its 2021 acquisition of Intel’s NAND business for $9 billion was one of the largest technology deals of that year, and it cemented SK Hynix as the clear global number two in memory. In my experience working across Korean industries, SK Hynix has a somewhat different corporate culture than Samsung — less rigid hierarchy, slightly more collaborative in how it engages with international partners, though both operate at an intensity that would surprise most Western colleagues.

What This Means When You Visit Korea

Most foreign visitors to Korea experience Samsung as the brand on their hotel television or the logo on a building in Gangnam. Few realize they’re standing in the country that manufactures the physical memory of the modern world.

The semiconductor clusters are not tourist destinations — Suwon’s Samsung Digital City and SK Hynix’s Icheon campus are operational industrial complexes, not open to casual visitors. But the fingerprints of the industry are everywhere if you know where to look: in the engineering graduate recruitment posters on university campuses, in the surprisingly high concentration of technical talent in the Pangyo district south of Seoul (Korea’s equivalent of Silicon Valley), and in the quiet confidence with which Korean business people in any industry talk about what their country has built.

If you want to understand why Korea has become so technologically advanced in such a short time, the semiconductor story is the most honest answer. Everything else — the Hallyu Wave, the K-pop industry, the world-class infrastructure — runs on a foundation of industrial capability and national discipline that the chip industry built first.

The Challenges Ahead

I’d be presenting an incomplete picture if I didn’t acknowledge the pressures the industry is currently navigating.

China is investing enormously in domestic semiconductor production and has made closing the gap with Korean firms a stated national priority. The gap in advanced chip technology remains significant, but China’s capacity for sustained long-term investment in strategic industries is not something Korea can afford to dismiss.

The demographic problem is real. Korea has the lowest birth rate in the world and the engineering talent pipeline that fed the semiconductor industry for decades is under pressure. The companies are investing in automation and AI-assisted design, but the human capital challenge is structural.

Geopolitical risk has become more visible since 2020. Korea sits between the United States and China in a way that requires constant, careful navigation — and both countries have significant interest in Korean chip supply chains. This is a dimension of Korean industrial life that occupies far more boardroom attention than most outsiders realize.

None of these challenges are fatal. But they’re real, and any honest account of the industry should say so.

FAQ

Who makes more chips — Samsung or TSMC? They make different types. TSMC (Taiwan) is the world leader in advanced logic chips — the processors that compute. Samsung and SK Hynix dominate memory chips — DRAM and NAND flash. Both are essential; they serve different functions in your device.

Can I visit Samsung’s semiconductor facilities in Korea? The production facilities are closed to the public. Samsung does operate the Samsung Innovation Museum in Suwon, which covers the company’s history and is open to visitors. It’s a worthwhile half-day if you’re interested in Korean industrial history.

Why does Korea dominate memory chips specifically? A combination of early government support, chaebol willingness to absorb losses through market downturns, and an engineering culture that prioritises production efficiency over everything else. The advantages compounded over decades into a near-structural dominance.

Is Korea’s semiconductor industry safe from Chinese competition? In the short term, yes — the technology gap in advanced memory production remains significant. In the medium term, it’s a question Korean policymakers and engineers think about very seriously. The honest answer is that nobody knows with certainty.

How does the semiconductor industry affect daily life in Korea? Significantly. The industry is the single largest contributor to Korean export revenue, which means its cycles — booms and downturns — ripple through the entire economy. When chip prices fall, Korean consumers feel it. When demand spikes, the country benefits broadly.

See Korea’s Industrial Story in Person

The semiconductor factories aren’t open for tours, but Korea’s transformation from war-torn peninsula to global technology powerhouse is visible everywhere — in its infrastructure, its cities, and its people. These experiences give you the best context.

Korea Insider has lived in South Korea for 50 years and worked at international companies for over two decades — explaining Korean culture, food, and society to colleagues from the US, Europe, and Australia.

Internationally married with a Japanese spouse, Korea Insider brings both an insider’s depth and an outsider’s perspective to every topic on My Korea Tip.